Protecting Your Assets: The Reality of Earthquake Insurance for California Commercial Properties

Earthquake insurance for California commercial property protects building owners against structural damage, business interruption losses, and liability exposure from seismic events that standard commercial property insurance explicitly excludes. California sits on or near more than 500 active fault lines, and the USGS estimates a 72% probability of a magnitude 6.7 or greater earthquake striking the state within the next 30 years. Despite this risk, fewer than 15% of California commercial properties carry earthquake coverage. We help commercial property owners evaluate their seismic exposure, compare coverage options, and structure policies that balance protection with cost. This guide covers the scope of commercial earthquake coverage, deductible structures, cost ranges, and the decision factors that determine whether this coverage makes financial sense for your property.

What Commercial Earthquake Insurance Covers

Commercial earthquake coverage provides three core protections that standard commercial property insurance does not: building structure repair or replacement, business personal property damage, and business interruption losses resulting from seismic events. Standard commercial property policies contain an explicit earthquake exclusion — meaning a magnitude 7.0 event that destroys your building generates zero recovery under your existing property policy.

Building coverage pays for structural repair or replacement when an earthquake damages the foundation, walls, roof, and permanently attached fixtures. Business personal property coverage extends to equipment, inventory, and contents damaged by the event. Business interruption coverage — a critical component for commercial properties — reimburses lost revenue and continuing operating expenses during the repair period, which can extend 6 to 18 months for significant structural damage.

The California Earthquake Authority (CEA) provides residential earthquake policies but does not offer commercial coverage. Commercial earthquake insurance must be obtained through the private surplus lines market or specialty commercial insurers, which provides more flexible coverage terms but requires careful evaluation of policy language and exclusions.

Key Takeaway: Commercial earthquake insurance covers building structure, business personal property, and business interruption losses that standard commercial property policies explicitly exclude — with commercial coverage available only through private insurers since the California Earthquake Authority does not cover commercial properties.

California Seismic Risk Context

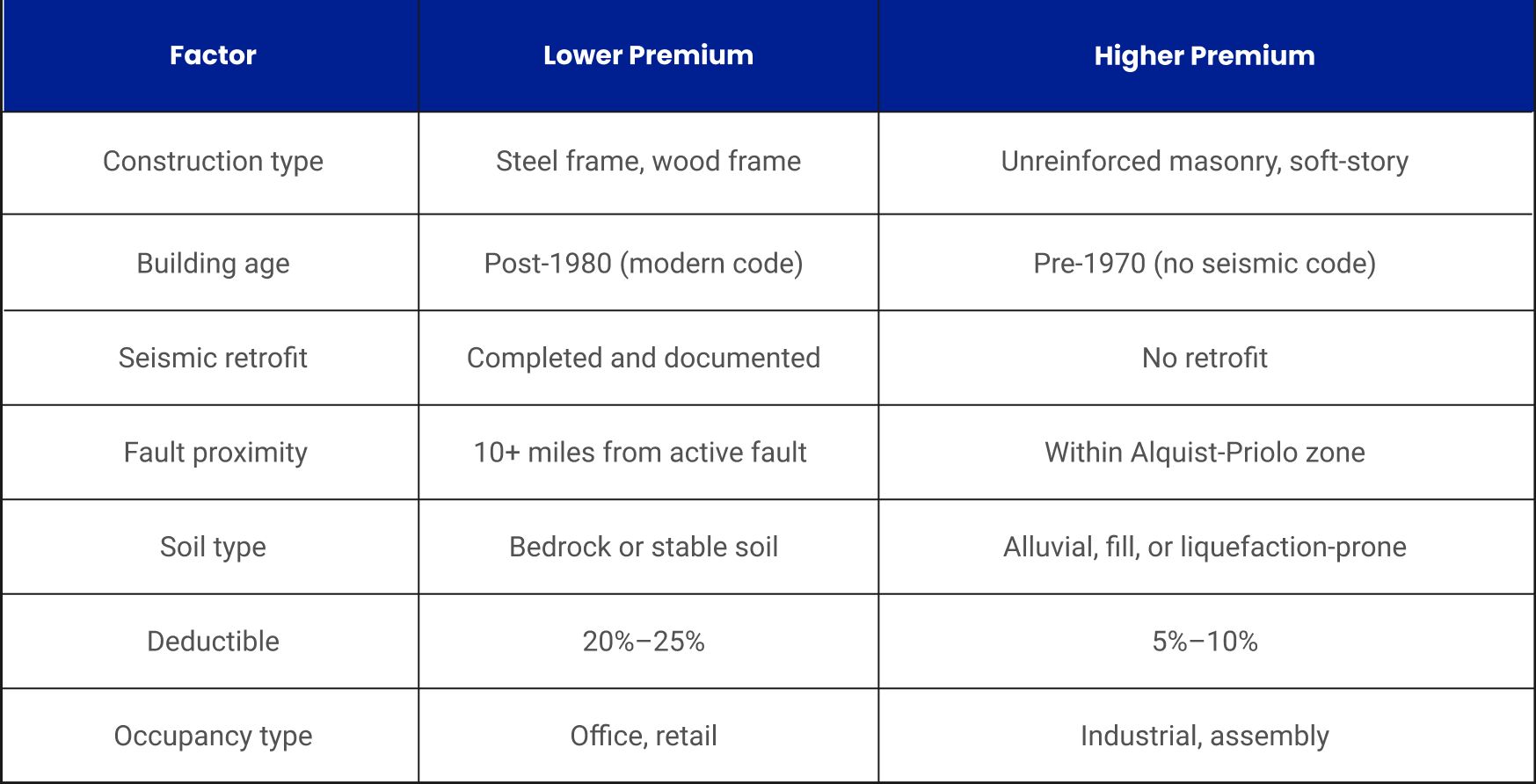

California's seismic risk profile directly influences earthquake insurance availability, pricing, and underwriting requirements. The state's major fault systems — the San Andreas, Hayward, and San Jacinto faults — create varying risk levels across different regions, and insurers use fault proximity, soil type, and structural risk assessment data to price policies.

Properties located within designated Alquist-Priolo Earthquake Fault Zones face the highest premiums and most restrictive underwriting. These zones map surface traces of active faults where fault rupture displacement is most likely. Commercial buildings within these zones may require seismic retrofit documentation or structural engineering reports before insurers will offer coverage.

Soil liquefaction risk — where saturated, loose soil loses structural integrity during seismic shaking — adds an additional risk factor that affects properties built on alluvial plains, filled land, and areas with high water tables. Coastal and bayside commercial districts in San Francisco, Oakland, and Long Beach carry elevated liquefaction risk that increases both premiums and deductible requirements.

Key Takeaway: California's seismic risk varies by fault proximity, Alquist-Priolo zone designation, and soil liquefaction potential — with properties in high-risk zones facing the highest premiums, most restrictive underwriting, and potential requirements for seismic retrofit documentation before coverage is available.

Earthquake Insurance Deductible Structures

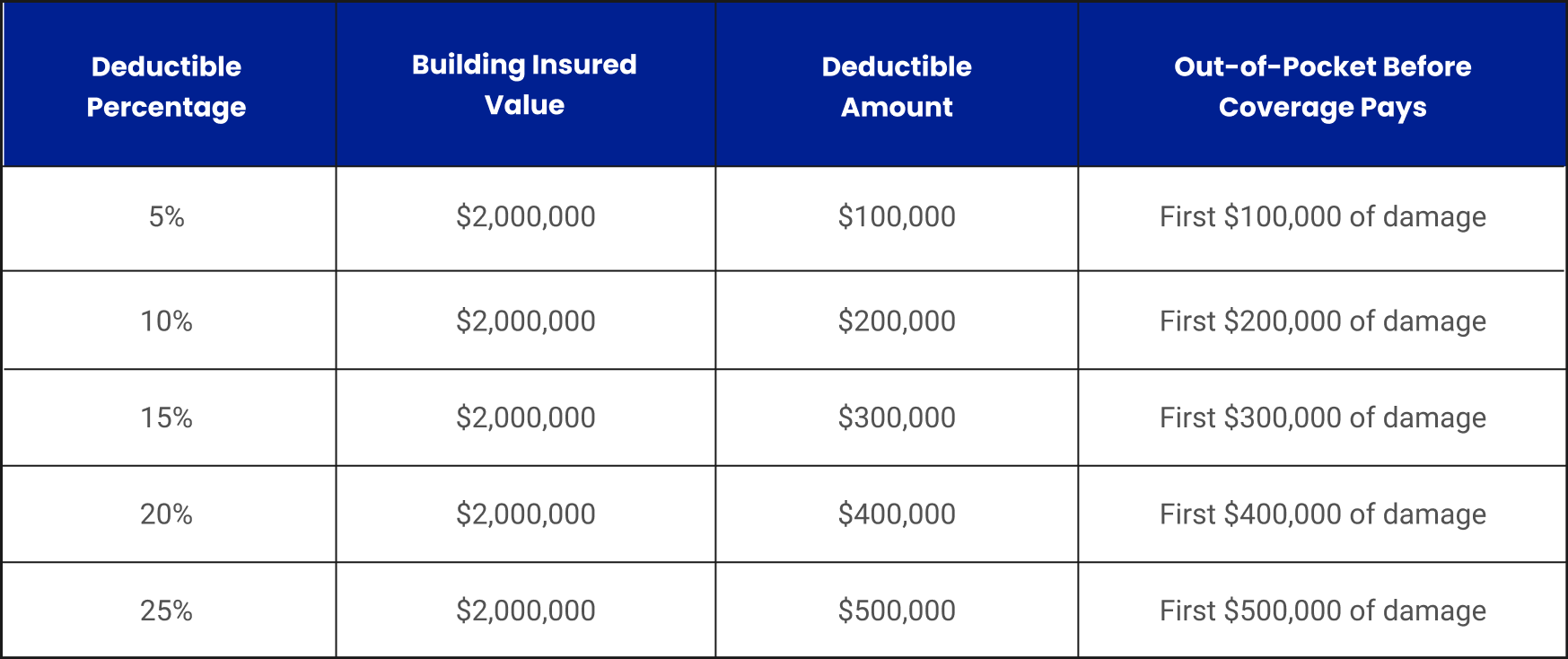

Earthquake insurance deductibles operate fundamentally differently from standard property insurance deductibles. Instead of a fixed dollar amount, earthquake deductibles are expressed as a percentage of the building's insured value — typically ranging from 5% to 25% of the coverage limit.

Lower deductible percentages reduce your out-of-pocket exposure but significantly increase annual premiums. A 5% deductible policy may cost 40% to 60% more than a 15% deductible policy on the same building. Most commercial property owners select deductibles in the 10% to 15% range as a balance between affordability and meaningful loss protection.

The deductible applies per-occurrence and typically applies separately to the building and contents coverages. Some policies also apply a separate deductible percentage to the business interruption component. Understanding this structure prevents the assumption that a "10% deductible" means a single 10% retention across all coverage categories.

Key Takeaway: Earthquake deductibles are percentage-based (5% to 25% of insured value), not fixed dollar amounts — a 10% deductible on a $2 million building means $200,000 out-of-pocket before coverage pays, with separate deductibles potentially applying to building, contents, and business interruption components.

How Much Does Commercial Earthquake Insurance Cost?

California earthquake insurance cost for commercial properties ranges from $1.50 to $8.00 per $1,000 of coverage annually, depending on location, building construction type, age, seismic retrofitting, and deductible selection. A $2 million commercial property in a moderate-risk zone with a 10% deductible can expect annual premiums of $5,000 to $12,000.

Unreinforced masonry buildings and soft-story commercial structures (with open ground-floor parking or retail beneath multiple upper stories) face the highest premiums — often 3 to 5 times the rate for comparable steel-frame or wood-frame buildings. Many insurers decline to cover unreinforced masonry without documented seismic retrofit.

We recommend obtaining quotes from at least three specialty commercial earthquake insurers and comparing not only premiums but policy language, deductible structures, business interruption sub-limits, and exclusions for land damage, sprinkler leakage, and fire-following-earthquake.

Key Takeaway: Commercial earthquake insurance costs $1.50 to $8.00 per $1,000 of coverage ($5,000 to $12,000 annually for a $2 million property), with construction type, building age, seismic retrofit status, fault proximity, and deductible selection as the primary pricing factors.

Decision Factors: Is Earthquake Insurance Worth It?

The decision to purchase earthquake insurance for California commercial property depends on five financial and operational factors specific to your property and business.

Replacement Cost vs. Deductible Gap — If your property's replacement cost is $3 million and your deductible is 15% ($450,000), you need to assess whether your business can absorb a $450,000 loss without catastrophic financial impact. If not, the premium is the cost of avoiding that scenario.

Mortgage Lender Requirements — Lenders on commercial properties in high-risk zones may require earthquake coverage as a loan condition. Even where not required, lenders may adjust terms if earthquake coverage lapses.

Business Interruption Exposure — A commercial property that generates $500,000 to $1 million in annual revenue faces significant interruption risk from a major earthquake. If your business cannot relocate quickly and the building requires 6 to 18 months of repairs, the lost revenue may exceed the building damage itself.

Portfolio Diversification — Property owners with multiple buildings across different seismic zones have natural diversification that reduces the catastrophic impact of any single event. Single-property owners face concentrated risk that insurance addresses directly.

Seismic Retrofit Investment — Properties with documented seismic retrofitting receive lower premiums and broader coverage availability. The retrofit investment reduces both the probability of severe damage and the ongoing insurance cost — often paying for itself within 5 to 10 years through premium savings.

Key Takeaway: Evaluate earthquake insurance by comparing the deductible gap to your financial reserves, assessing business interruption revenue exposure ($500,000+ annual revenue properties face significant risk), checking lender requirements, reviewing portfolio concentration, and factoring seismic retrofit premium savings into the cost-benefit analysis.

Frequently Asked Questions

Is earthquake insurance worth it in California?

Earthquake insurance is worth evaluating for any California commercial property that cannot self-insure against a 10% to 25% deductible loss. Properties in high-risk zones, single-asset portfolios, and businesses with significant revenue at risk from interruption benefit most from coverage.

How much does commercial earthquake insurance cost?

Annual premiums range from $1.50 to $8.00 per $1,000 of coverage — approximately $5,000 to $12,000 per year for a $2 million property with a 10% deductible. Costs vary by construction type, building age, seismic retrofit status, and fault proximity.

What does earthquake insurance cover for businesses?

Commercial earthquake insurance covers building structure repair or replacement, business personal property (equipment, inventory), and business interruption losses. Standard commercial property insurance explicitly excludes earthquake damage — this is separate, additional coverage.

What is the typical earthquake insurance deductible?

Earthquake deductibles are percentage-based, typically 10% to 15% of the insured value for commercial properties. A 10% deductible on a $2 million building means $200,000 out-of-pocket before coverage applies. Lower deductibles increase premiums by 40% to 60%.

Does regular commercial insurance cover earthquakes?

Standard commercial property insurance contains an explicit earthquake exclusion. Fire following an earthquake may be covered under the standard policy, but structural damage, contents loss, and business interruption from the earthquake itself require a separate earthquake policy.

Make an Informed Coverage Decision

Earthquake insurance for California commercial property addresses a risk that standard coverage explicitly excludes — and the state's seismic activity makes this gap one of the highest-exposure coverage decisions commercial property owners face. The right policy balances deductible tolerance, premium cost, and business interruption protection based on your property's specific risk profile.

We specialize in helping commercial property owners evaluate their seismic exposure, compare coverage options across multiple specialty insurers, and structure policies that protect assets without overpaying. Schedule a Consultation to review your property's risk profile and receive a customized coverage recommendation.